Self-Employed Workers Have to Pay Both the Employer and Employee Contributions

In Canada, self-employed workers have pay “double” for CPP because they are on the hook for both the employer and employee portions of the premiums.

This is nothing new; and its one of the disadvantages of being self-employed in Canada.

Self-Employed Canadians Now Paying 11.9% of their Salary Towards CPP

What is new are the CPP2 and enhanced CPP contribution programs.

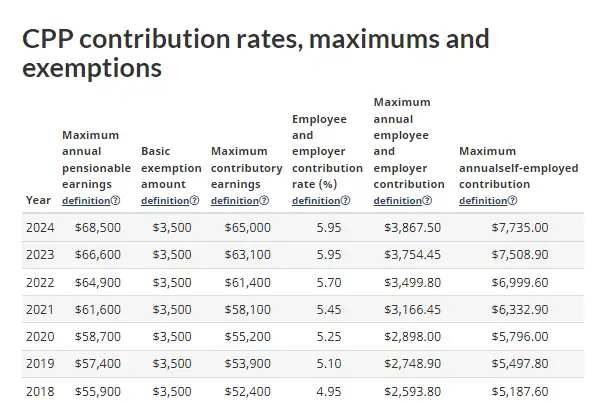

Under these initiatives, CPP contributions in Canada have gone from 4.95% (from both the employee and employer) up to 5.95% each.

Not only has the contribution percentage increased, but the earnings ceiling has increased $13,000 between 2018 and 2024 as well — so, Canadians are paying a higher percentage on more money.

As mentioned, self-employed Canadians have to pay both contributions, meaning this year, self-employed Canadians now have to pay 11.9% of their salary towards CPP up to $68,500….

……but, we’re not quite at the $8,760 quoted in the title yet. There’s more!

Enter CPP2

The Government has also introduced another new CPP program recently, creatively named CPP2.

This program adds further CPP premiums for employees and employers in Canada.

Under this program, self-employed Canadians will have to pay additional CPP contributions of $376 in 2024 and $776 (estimated) in 2025.

Total CPP Bill in 2025? – $8,760

Using some simple math, adding a 3% indexing increase to base CPP, and then using the CPP2 estimates provided by the government, we can estimate that CPP premiums for a self-employed Canadian making $79,400 in 2025 will be $8,760. Yikes!

This is on top of the estimated $21,000 income tax they would owe. (Ontario, using no write-offs but CPP and EI. Consult a pro to finalize your numbers.)

Unlike Professional Self-Employed Canadians, Gig Workers Can’t Dodge This One

Professional Canadians who are incorporated will be able to “dodge” this CPP increase by paying themselves dividends. (there’s benefits and drawbacks to this)

Gig workers, being sole-proprietors, do not have this option. CPP is mandatory for them at tax time, and the CRA is not who you want to owe money to.

(they charge 10% interest on late payments, as of writing this article)

Of Course, You’ll Get More Money When You Retire

These additional CPP contributions dont just disappear into thin air; you’ll be entitled a larger pension when you retire, but that is beyond the scope of this article. Here is a good resource for determining what you could get.

Despite receiving more money in the future, one thing is for sure — Canada’s most vulnerable workers will be receiving large CPP bills going forward.

Bills which certainly wont help them with their absurdly expensive short-term basic needs.