Home Insurance is up. Alot.

While everyone has been fixated on car insurance premiums, the cost of homeowner’s insurance has been creeping up.

Well, its not really a creep, its more of a rocket-launch.

Since the year 2000, homeowner’s insurance has almost quadrupled in Canada, according to Stats Canada data.

Yes you read that right. QUADRUPLED. From a CPI index of 88 in 2000, to 330 in 2024. (orange line, below)

This is significantly higher than inflation which is up 52% during that time period (blue line below)

Cost of Materials, Labour and Weather Events to Blame

It all comes down higher input costs according to industry experts.

“The cost of materials, labour, and homes has increased significantly in the last few years, as has the heightened frequency and severity of natural disasters. Annual catastrophic lossess in excess of $2 billion have become common” says a recent press release from CatIQ, and insurance industry publication.

These Costs Affect Homeownership CPI, Which in Turn Keeps Interest Rates High

These increases create a vicious feedback loop. As insurance rates surge, they force Stats Canada’s shelter CPI up, shelter CPI pushes headline CPI up, and interest rates stay high.

In short, high costs keep interest rates high, and the net effect is that homeownership falls further out of reach of prospective homebuyers.

Tenant’s Insurance not Seeing the Same Price Increases

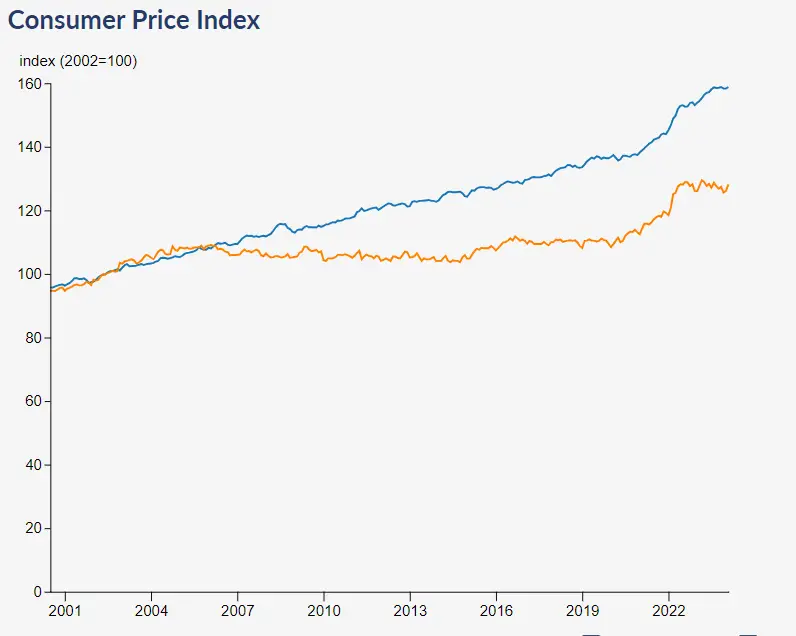

Tenant’s insurance (orange line) has trended below CPI (blue line) since the year 2000.

Unfortunetly though, their landlords are likely passing on their building insurance in the form of rent increase.

This means that renters do feel the cost of homeowner’s insurance on top their tenants insurance.