Somebody Do a Wellness Check on the CMHC, Because Their Cashflow Must be Down

Quick primer: Insured mortgages in Canada usually means mortgages with smaller downpayments. The important part is that these mortgages include an insurance premium — a premium which is usually paid to the CMHC to cover the lender in case you default.

Insurance companies need premiums to keep the lights on — the problem for the CMHC is that not very many people are paying these premiums these days.

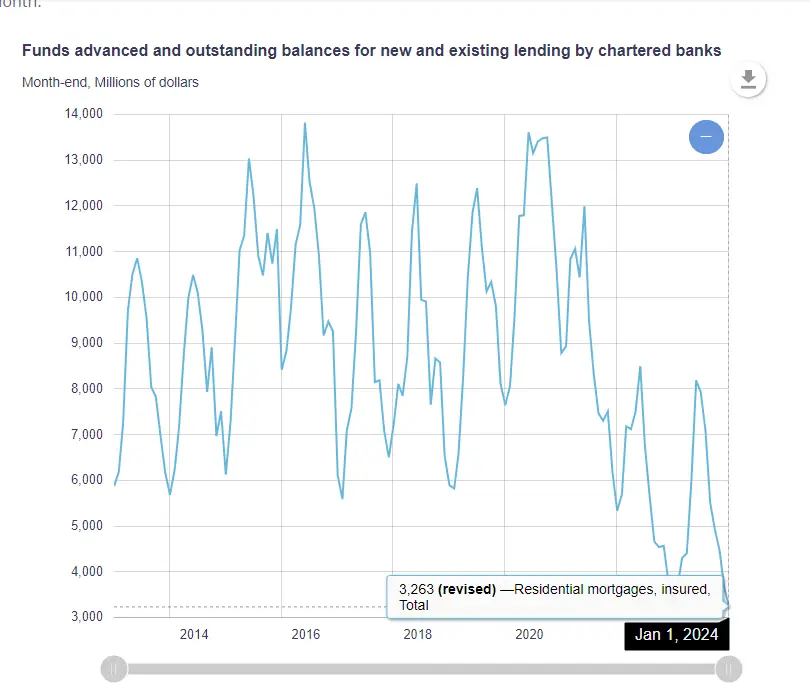

In fact, only $3.2B dollars in insured mortgages were lent out by Chartered banks in all of Canada in January 2024.

This is the lowest print since records began in 2013.

This comes only days after the government of Canada announced that it would buy 50% of all CMHC bonds issued in 2024.

Additionally, this all occurred around the same time major banks started calling for the BoC to exclude shelter CPI components from their preferred core inflation metrics.

With over $2T in mortgage loans outstanding, the mortgage industry in Canada is massive, and you can be sure that alot of people must not be happy with these numbers.

Uninsured Mortgage Lending on Life Support as Well

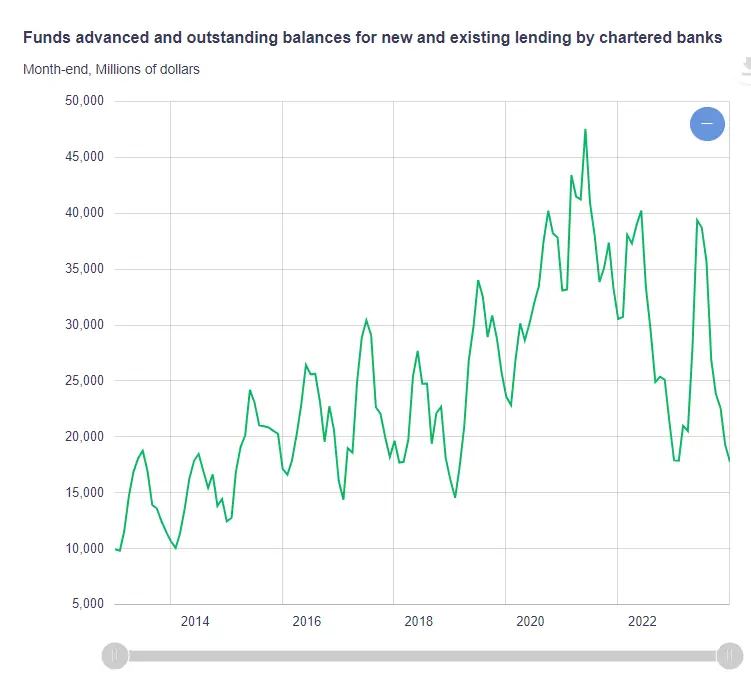

Not only were insured mortgages struggling in the early part of 2024, uninsured mortgage lending was on life-support as well.

At only $17.6B lent out in Jan. 2024, uninsured mortgage lending is also flirting with multi-decade lows.

These numbers are abysmal, watch for stress in the mortgage sector.